Introduction

Every year, millions of young people graduate from high school having studied quadratic equations, the causes of the First World War, and the chemical composition of water — and having received almost no instruction on how to manage the money they are about to earn, borrow, and spend for the rest of their lives.

They will open bank accounts, take on student loans, sign lease agreements, apply for credit cards, and eventually navigate mortgages, retirement accounts, and tax obligations — all without having been formally taught what any of these things mean or how to use them wisely. The consequences of this gap are not abstract. They show up in credit card debt accumulated in the first years after graduation, in student loans that compound for decades because borrowers did not understand the repayment terms they agreed to, in retirement savings that are started too late or not at all.

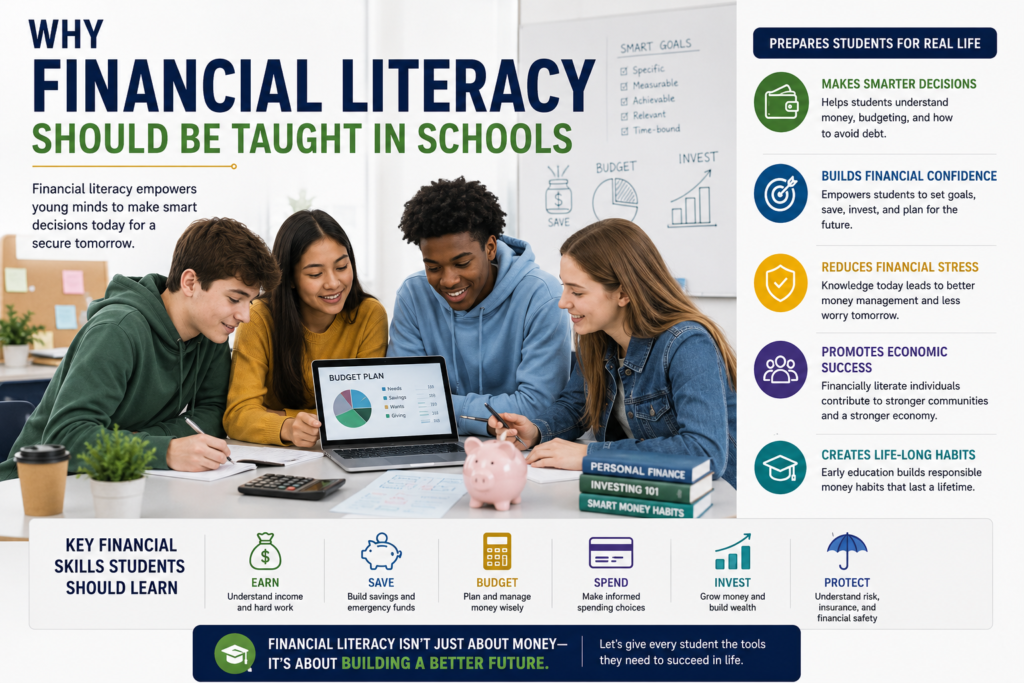

Financial literacy — the ability to understand and effectively use financial skills, including personal budgeting, saving, investing, debt management, and understanding financial products — is not a specialized professional skill. It is a life skill, as fundamental to functioning in modern society as reading or arithmetic. And yet it remains, in most school systems around the world, an afterthought at best and an absence at worst.

This article makes the case that financial literacy education belongs in schools — not as an elective, not as a module tucked inside a home economics class, but as a core, compulsory part of every student’s education.

The Scale of the Problem

Before arguing for a solution, it is worth being precise about the problem. The data on financial literacy — and on the financial behavior that flows from it — is sobering.

A global survey conducted by Standard & Poor’s in partnership with the World Bank, covering more than 150,000 adults across 140 countries, found that only one in three adults worldwide is financially literate. In the United States, often assumed to be a financially sophisticated country, only 57 percent of adults met the basic definition of financial literacy used in the survey. In the United Kingdom, the figure was 67 percent. In developing economies, the numbers were frequently below 30 percent.

The consequences are visible in the aggregate data. Household debt in most developed countries has reached historic highs. In the United States, total household debt exceeded $17 trillion in 2023. Credit card debt alone surpassed $1 trillion for the first time — much of it carried by people paying interest rates of 20 percent or more, often without fully understanding the compounding mechanics that make high-interest debt so destructive.

Retirement preparedness is equally alarming. Studies consistently show that large proportions of working-age adults have little or no retirement savings. A significant portion of people approaching retirement age have saved less than $50,000 — a figure that would cover perhaps two years of modest living expenses. The reasons are complex, but a recurring theme in the research is that people did not understand, early enough, how compound growth works and why starting early matters so dramatically.

Student loan debt represents another dimension of the crisis. In the United States alone, outstanding student loan debt exceeds $1.7 trillion, held by roughly 45 million borrowers. Many of those borrowers took on debt they did not fully understand — signing loan agreements at 17 or 18 without a clear picture of total repayment costs, interest accrual during deferment, or the relationship between their chosen field of study and their likely earning capacity.

These are not failures of individual intelligence or willpower. They are, in large part, failures of education.

What Financial Literacy Actually Covers

There is sometimes a misconception that financial literacy means teaching students how to get rich, or how to pick stocks, or how to “win” at personal finance. This misunderstands the subject.

At its core, financial literacy covers a set of practical competencies that every adult needs regardless of income level, career, or ambition:

Budgeting and cash flow management. Understanding the difference between income and expenses, tracking where money goes, and making deliberate decisions about how to allocate limited resources. This sounds elementary, but surveys consistently show that large numbers of adults cannot accurately describe their own monthly spending, and many have no system for managing their cash flow at all.

Saving and the concept of an emergency fund. Understanding why saving is necessary, how much to save, and what an emergency fund is and why it matters. Research shows that a significant proportion of adults in developed countries could not cover a $400 emergency expense without borrowing money or selling something. The absence of even a basic financial buffer makes people extraordinarily vulnerable to ordinary setbacks.

Understanding credit and debt. How credit cards work, what interest rates mean, how compound interest functions on debt, what a credit score is and how it is determined, and the long-term consequences of carrying high-interest debt. Understanding the difference between good debt (which funds appreciating assets or income-generating activities) and bad debt (which funds consumption) is fundamental to adult financial health.

Compound growth and investing basics. Understanding that money invested over time grows exponentially, not linearly — and that the starting age for investment matters enormously. A person who begins investing $200 per month at age 22 will retire with dramatically more wealth than one who begins at 32, even if the later starter contributes for more years. This is one of the most powerful and least-understood concepts in personal finance.

Banking and financial products. Understanding how bank accounts work, what fees to look for, how loans and mortgages are structured, what insurance is and why it matters, and how to read a financial statement or contract. Most young adults sign financial agreements — lease contracts, loan documents, insurance policies — without fully understanding what they are agreeing to.

Taxes. Understanding how income tax works, what a tax return is, what deductions and credits are, and how to file a basic return. Tax literacy is particularly poor even among educated adults, and the consequences of ignorance — missed deductions, penalties, failure to take advantage of tax-advantaged savings vehicles — can be significant over a lifetime.

None of this is advanced. None of it requires mathematical sophistication beyond basic arithmetic and an understanding of percentages. What it requires is deliberate instruction, time to practice, and a curriculum that takes the subject seriously.

Why Schools Are the Right Place for This Education

One common response to the case for school-based financial literacy is that this is the family’s responsibility. Parents should teach their children about money. Schools are for academic subjects.

This objection fails on several grounds.

Not all families have the knowledge to teach it. Financial literacy, as the data shows, is not widespread among adults. A parent who does not understand compound interest, who has never had a retirement account, who manages debt poorly — this parent cannot reliably transmit financial knowledge to their children regardless of their good intentions. The cycle of financial ignorance reproduces itself generationally unless it is interrupted by formal education.

Not all families have the conversations. Even in families where the parents are financially literate, money is often treated as a private or uncomfortable topic. Many adults grew up in households where financial matters were not discussed openly, and they carry that reticence into their own parenting. Children in these families absorb habits and attitudes about money without ever receiving explicit instruction.

Financial outcomes correlate strongly with family background — and schools can break that correlation. Research on financial literacy education consistently shows that formal instruction in schools is particularly beneficial for students from lower-income backgrounds, who are less likely to have received financial knowledge at home and who are more likely to face financial decisions with significant consequences at a young age. The school is one of the few institutions capable of providing equitable access to this knowledge regardless of family wealth or educational background.

The school is where foundational life skills belong. We teach students to read, not because we assume their families will not read to them, but because literacy is a foundational competency that society has decided every person needs and every child deserves. The same logic applies to financial literacy. A person who cannot read is disadvantaged in almost every dimension of modern life. So is a person who cannot manage money — the consequences are simply less visible and accumulate more slowly.

The Evidence on What Works

There is genuine debate among researchers about whether financial literacy education, as it is typically implemented, actually changes behavior. Several large reviews have found modest or mixed effects, and critics have used this evidence to argue that school-based financial education is ineffective.

This critique deserves a serious response, because it is partly right and partly wrong.

The evidence for poorly designed financial literacy programs — one-time seminars, checkbox modules, abstract instruction disconnected from any real decisions — is indeed weak. Knowledge alone does not reliably change behavior. A student who attends a 45-minute presentation on credit cards and then returns to a life in which no financial decisions are discussed, practiced, or reinforced is unlikely to be meaningfully changed by the experience.

But the evidence for well-designed programs is considerably more encouraging. Research on sustained, integrated financial education — programs that span multiple years, connect concepts to real decisions, involve practice and application, and engage students around their own actual financial situations — shows meaningful effects on savings behavior, credit use, and financial planning.

A 2014 study examining states in the United States that mandated financial education in high schools found that students in those states were significantly more likely to save, less likely to carry high-interest debt, and had higher credit scores as young adults than comparable students in states without mandated financial education. The effects were larger for lower-income students — precisely the population most likely to face the consequences of financial ignorance.

Studies of retirement savings programs — particularly those that include an educational component alongside automatic enrollment — show that understanding how compound growth works, and what an employer match means, substantially increases participation rates. This is a direct behavioral outcome of financial knowledge, not just an attitudinal one.

The lesson from the mixed evidence is not that financial literacy education does not work — it is that it must be done well. Depth matters more than coverage. Practice matters more than information transfer. Sustained engagement matters more than one-time exposure. These are not unique insights about financial education; they describe good education generally.

What a Good Financial Literacy Curriculum Looks Like

For financial literacy education to be effective, it cannot be an add-on or an afterthought. It needs to be thoughtfully designed, appropriately sequenced, and embedded in a broader educational experience that connects abstract concepts to real decisions.

Start early and build progressively. Elementary students can learn about earning, saving, and spending. The concept of a trade-off — that spending money on one thing means not having it for another — is accessible to young children and lays the groundwork for more complex concepts later. Middle school is the appropriate time to introduce budgeting, banking basics, and the concept of interest. High school is where compound growth, credit, debt, investing, and tax literacy belong.

Connect concepts to real decisions. The most effective financial education involves students making actual or simulated decisions with real stakes. Budgeting exercises that use realistic income and expense figures — rather than round numbers pulled from nowhere — force students to confront genuine trade-offs. Simulated investment portfolios that track real market performance over the course of a school year teach compound growth more effectively than any lecture.

Include the behavioral and psychological dimensions. Financial decisions are not made in a vacuum of pure rationality. They are shaped by emotion, social pressure, cognitive bias, and habit. An effective financial literacy curriculum addresses these realities — teaching students about present bias (the tendency to overvalue immediate rewards relative to future ones), loss aversion, the psychological difficulty of delaying gratification, and the social dynamics around spending and consumption. This is arguably more important than teaching the mechanics of a mutual fund.

Use qualified instructors. There is a genuine challenge here. Many classroom teachers have not themselves received financial education and feel uncomfortable teaching a subject in which they lack confidence. Effective financial literacy education requires investment in teacher training or the use of specialized educators. Some schools have addressed this by partnering with financial professionals, credit unions, or nonprofit organizations that provide both curriculum and instruction.

Assess genuine competency, not just knowledge recall. Testing whether a student can define “compound interest” is not the same as testing whether they can apply it to a real scenario — whether they can calculate the true cost of a loan, or compare the long-term returns of different savings strategies. Assessment should demand application, not just recall.

Addressing the Counterarguments

“There’s no room in the curriculum.” Every generation of educational reform encounters the objection that the curriculum is full and new subjects cannot be added without removing something else. This argument has some validity — curriculum time is genuinely limited, and choices must be made. But it also reflects a set of existing priorities that deserve scrutiny. Financial literacy is not competing with calculus or literature for the title of most academically prestigious subject. It is competing with a genuine and demonstrable need. Many schools find space by integrating financial literacy content across existing subjects — mathematics classes that use financial examples, social studies classes that address economic history and policy, English classes that analyze persuasive financial marketing.

“Technology will handle this.” Some argue that budgeting apps, robo-advisors, and automated financial tools make financial literacy less necessary — that people can simply let technology manage their finances without needing to understand the underlying principles. This argument underestimates how much understanding is required to use financial technology wisely. An app can track spending, but it cannot tell you whether your spending reflects your values. A robo-advisor can allocate investments, but it cannot explain why you should be investing in the first place, or help you resist the impulse to withdraw everything when the market falls 20 percent. Financial technology is a tool; understanding what to do with it still requires financial literacy.

“It should be the parents’ job.” As argued above, this position is both empirically unjustified and ethically unsatisfying. We do not leave the teaching of reading, mathematics, or civic knowledge to parents on the grounds that it is their responsibility. We recognize that these competencies are too important and too foundational to depend on the accident of what family a child happens to be born into. Financial literacy deserves the same recognition.

The Broader Social Case

The argument for financial literacy in schools is not purely about individual welfare. There is a broader social case that deserves acknowledgment.

A financially literate population is more economically stable. People who understand debt are less likely to take on more than they can service, contributing to the kind of over-leveraging that amplifies the severity of financial crises. People who understand saving and investment are better prepared for retirement, reducing dependence on public pension systems under demographic pressure. People who understand basic insurance are better protected against catastrophic risk and less likely to require public assistance in the event of illness or accident.

A financially literate population is also more resistant to exploitation. Predatory lending, payday loan schemes, multi-level marketing operations, investment fraud, and aggressive credit card marketing all depend, to a significant degree, on the financial ignorance of their targets. Financial education does not eliminate exploitation, but it raises the cost of it — a population that understands interest rates and reads the fine print is a harder population to exploit.

Finally, financial literacy intersects with civic literacy in ways that are increasingly important. Questions about monetary policy, government debt, social security reform, and financial regulation are central to democratic politics. Citizens who lack a basic understanding of how financial systems work are poorly equipped to evaluate the economic arguments that shape political debate — and are correspondingly more vulnerable to demagogic simplifications on all sides.

Conclusion

The case for teaching financial literacy in schools does not rest on any single argument. It rests on the convergence of several facts: that financial decisions are among the most consequential choices most people make; that the knowledge required to make them well is not instinctive but learnable; that many families cannot or do not provide this education; that the consequences of financial ignorance fall disproportionately on those who are already most vulnerable; and that school-based education, when well designed, demonstrably improves financial outcomes.

We live in a world in which the complexity of financial products and the sophistication of financial marketing have outpaced the financial knowledge of ordinary people. The gap between what the financial industry understands and what its customers understand is not a law of nature. It is a policy choice — one that reflects what we have decided to teach and what we have decided to leave to chance.

Young people deserve better than chance. They deserve an education that prepares them for the financial realities they will face — the debts they will consider taking on, the savings decisions they will need to make, the contracts they will be asked to sign. Teaching them to navigate these realities is not optional. It is one of the most practical and consequential things a school can do.